Understanding your financial situation will give you a sense of control over your life – before, during, and after divorce.

By Fadi Baradihi, MBA, CFP®, ChFC®, CLU, CDFA®

When contemplating divorce, most people put themselves under undue stress worrying about their financial well-being. Much of that stress is due to the fear of the unknown. So what do you do about it? Before, during, or after a divorce, it is important to keep yourself in reality as to your financial situation. Doing so will give you a sense of control over your life, which will reduce your stress level. Your financial situation can be broken into four different categories: assets, liabilities, income, and expenses. The following are some tips on how to effectively do that.

Assets

Assets have a way of disappearing after divorce proceedings start. As soon as divorce becomes a possibility, start by listing what assets you think the two of you own. That list would include:

- Cash. Do you keep any at home or in a safety deposit box?

- Checking account. The list would include personal, joint, business, or trust accounts.

- Savings or money-market accounts. Don’t forget accounts set up for a “special purpose” such as Christmas club or annual or semiannual expenses. Those accounts are usually funded by payroll deduction and are set up to fund large and infrequent expenses such as the annual premium on the home or auto insurance, Christmas, and so on. Those accounts are easy to forget.

- Retirement accounts. These include IRAs, RRSPs, defined contribution plans and pension plans (government and private). Don’t forget any plans from previous employers that were left behind.

- Non-retirement investment accounts. These include mutual funds, brokerage accounts, annuities, cash-value life insurance, certificates of deposit, and stocks or bonds held in certificate form.

- Real estate. This usually consists of the house and any other property owned by the couple.

- Employer-funded incentive programs. These could include stock-option programs, country- club initiation fees, banked vacation, and sick days.

Once you have your completed list, start collecting statements for every item on it. Investment companies send statements monthly or quarterly, depending on the type of account, the level of trading activity, and the company’s policy. Most employer-sponsored plans send out a year-end statement in the first quarter of the following year. So don’t panic if a statement you’re looking for doesn’t show up at the end of the first month after you start the process. If you have a safety deposit box and you don’t have a list of its contents, visit the bank and make a list. Lastly, make a copy of the last mortgage closing paperwork. In order to qualify for a mortgage, you would have to disclose all of your assets, liabilities, and sources of income and the last five years’ tax returns. Tax returns will show the sources and amount of income, especially if your spouse is self-employed.

Liabilities

Liabilities, unlike assets, have a way of appearing when divorce is pending. Other than listing liabilities, keep track of excessive increases in debt levels. If you see that happening, notify your lawyer immediately. As a general rule, any debt associated with an asset should travel with it. For example, whoever gets the car should get the car loan. If there’s a business involved, always question any debts to relatives, friends, employees, and especially the owner spouse. If you detect such a loan, ask for a signed loan agreement, what the purpose of the loan is, and a payment plan.

Income

The next step is to identify the sources of income. Income includes revenue from full- and part-time employment, investment return, and self-employment income. Add up all the income from different sources to come up with total income.

Your and your spouse’s income level is a factor in calculating child support and plays a role in arguing for alimony. Beware of close-relationship employers. I had a client who didn’t understand why her husband’s income was cut in half after he filed for divorce. After all, he worked for his brother’s construction company.

Expenses

The next step is to figure out your current budget and your post-divorce budget. Remember that the same amount of income supporting one household will need to support two.

The first step is to gather the necessary documentation that you would need in order to be objective. You should review your check register and credit-card statements. As you list your expenses, make sure you don’t “double dip.” For example, if your cell phone bill is directly charged to your credit card, don’t count your cell phone bill and the credit-card payment. An area that most people miss is cash withdrawals using ATM cards. You should be able to account for where that money was spent. When working on a budget, a good rule of thumb is to both have a number in each category and have a trusted and objective friend criticize your inputs. Start with the pre-divorce scenario using the one-page Expense Worksheet as a guide.

Using two copies of the Worksheet, fill in pre-divorce expenses and post-divorce expenses. Go to the post-divorce chart and carry over each expense with an increase or decrease in its value. For example, an increase would be lawn care, if you would need to hire it out. Food, on the other hand, would decrease.

Now you’re ready for your lawyer. You have a list of your assets, income, and expenses.

Example: John and Jane Smith

Let’s look at an example to see how it all fits in. John and Jane Smith are 40 years old and have two children. They own a home worth $165,000 with net equity of $77,500. Their retirement accounts total $165,500 in value. John earns $90,000 a year and has take-home pay of $68,760 a year. Jane has never worked outside the home and has no job skills, but she hopes to get a job with take-home pay of $8,900 a year.

The following settlement has been suggested. After the divorce, Jane and the children will live in the marital home, which will be deeded to her. She will also receive $44,000 of the retirement money and John $121,500, thus dividing the assets equally. John will pay Jane alimony of $600 per month for five years and child support of $225 per month per child. He will also pay college costs, which start in four years.

John’s expenses include his normal living expenses, child support, alimony, and college costs. Jane’s expenses include support for the children and are reduced when each child leaves home.

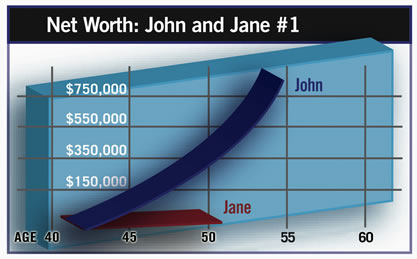

This appears to be a reasonably fair settlement. However, an analysis creates the financial future illustrated in Graph #1.

Jane’s assets will be completely depleted within seven years while John’s investments will grow dramatically. The reason is that, soon after the divorce is final, she will need to tap into her assets to make ends meet. She could have anticipated this situation had she done her homework.

To improve Jane’s financial future, the settlement could provide her with increased alimony of $1,500 per month for 10 years. After all, a major consideration for determining alimony or separate maintenance is the need of one spouse and the other’s ability to pay. Both numbers are a result of income minus expenses.

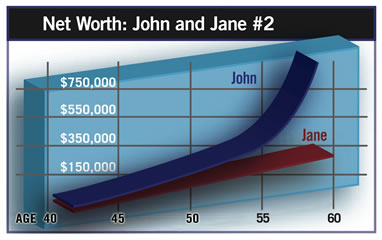

The correct child support, according to the Child Support Guidelines in their state/province, is $1,125 per month for two children for a couple with their income. Jane also could be awarded an additional $24,300 from the retirement plans. She may also need to cut her expenses by 10%. These changes in the original settlement will produce the results illustrated in Graph #2.

John will still have a surplus, which he can add to his investments. If John stays within his budget and invests all of his extra income, his investments have the capacity to grow to $2.5 million by the time he is 60.

This example illustrates the value of preparation as a means of reaching a more financially equitable divorce settlement. If the court’s intent is to treat both parties in a divorce as equitably as possible, it is essential to analyze the marriage as if it were a financial contract, with tangible investment into it by both parties. Without preparation, though, they wouldn’t have been able to argue for more alimony or an uneven split of assets.

For more information about how a CDFA® can help you with the financial aspects of your divorce, call (800) 875-1760