800.875.1760

800.875.1760

The role of the CDFA® (Certified Divorce Financial Analyst®) professional is to assist the client and his/her lawyer to understand how the financial decisions he/she makes today will impact the client’s financial future.

After his divorce, David went to a financial advisor to determine how to best position his assets. Together, David and his planner decided to do a total financial plan for him. During the planning session, it became apparent that during his marriage his wife had done all of the investing. She chose all the investments, made all the decisions, and invested all the money.

At the time of their divorce she said, “Let’s just split everything 50/50. You take this half of the assets and I will take that half. Is that OK?” David answered, “Well, I guess that sounds pretty fair. That’s OK with me.”

Unfortunately, there was something he neither knew nor understood; neither did his lawyer, and neither did the judge. They didn’t realize that David would have to pay taxes on his half of the assets when he tried to access them. His ex-wife, on the other hand, could access her half of the assets tax-free. His 50/50 split cost him an additional $18,000 in taxes. Had David met with a CDFA® (Certified Divorce Financial Analyst®) before the divorce was finalized, he would have been in a better position to ask for a more equitable settlement.

This parable has an unfortunate ending, but pre-divorce financial counseling can help people going through a divorce arrive at a settlement that is fully understood by all involved.

Who do people turn to for such assistance? When people think about getting a divorce, the first professional that comes to mind is an attorney. Typically a financial advisor – whether it is a CPA, CFP®, or a CDFA® – is not considered until later in the divorce process – or even until after the divorce is final.

Financial problems can tear a marriage apart, and are often the primary factor that leads to divorce. Once a decision to separate or divorce has been reached, all sorts of questions bubble to the surface. These questions are often clouded by wounded emotions and accompanied by mutual accusations, which comes as no surprise. If a couple cannot solve their financial difficulties while the marriage was underway, it is unlikely that they will be able to agree on pressing financial issues when it has fallen apart.

Many divorcing couples have questions such as:

• Where will the children live?

• Who will pay for their education and medical treatment?

• How do we value our property?

• Who gets what property?

• What tax issues must we be concerned with?

• How do we divide retirement funds and pensions?

• How will the lower-earning spouse survive financially?

• What additional financial support does that person need?

• Who gets the house?

• What happens if a paying ex-spouse dies?

These are the questions that divorce lawyers face with each divorce case. Many lawyers struggle with the intricate financial details that concern tax issues, CRA rulings, capital gains, dividing pensions, and so on. Lawyers attend law school to become experts in the law, not to become financial experts. Additionally, even if lawyers happen to have accumulated a degree of financial expertise, they are not allowed to testify on behalf of their clients in court. This is why more and more lawyers have seen the virtue of bringing a financial expert into the divorce process at the very start. Solid information and expert analysis are important resources in their search for the best possible resolutions for their clients.

Fortunately, with CDFA professionals, help is on the way.

What is the CDFA® (Certified Divorce Financial Analyst®) Professional's Role?

To understand this role, we first have to distinguish between a CDFA® (Certified Divorce Financial Analyst®) and other financial experts, who go by various titles, such as: Chartered Accountant (CA), Certified General Accountant (CGA), Certified Financial Planner® (CFP®), and Chartered Financial Consultant (ChFC®).

Financial Planners Help Clients Achieve Goals

The role of the financial planner, CFP® or ChFC® is to help people achieve their financial goals regardless of whether they are divorcing or happily married. After identifying those goals, the next step is to take an inventory of the clients’ current assets and liabilities, then examine what must be done to achieve those goals. Some goals might be reached within a year; others could be realized 50 years down the line. To look that far into the future, certain assumptions must be made. These include income, expenses, inflation rates, interest rates and rates of return on investments. After these assumptions are settled on and adjusted for changes, the scenario must be reviewed on a regular basis. If during the review process the planner determines that the client is not on track, he or she will recommend a number of necessary or advisable fine-tunings. In other words, the financial planner looks at financial results in the future based on certain assumptions made today, and keeps the client moving toward stated objectives.

Accountants Examine Details for Present Day

Conversely, accountants typically confine themselves to examining the details of a present-day scenario. If called upon to participate in a divorce proceeding, they might calculate the taxes on dividing property combined with the effect of child support and spousal support over a very short period of time. They typically do not project further into the future. They also may be retained to perform an audit of account activity or to perform forensic accounting functions to help uncover “hidden assets".

CDFA’s Responsibilities and the Team Approach

To best meet the needs of a divorcing client a blend of these two ideologies is needed. To meet this need a new professional designation was created – the Certified Divorce Financial Analyst®. The role of the CDFA® is to help both client and lawyer understand how the financial decisions made today will impact the client’s financial future, based on certain assumptions.

A CDFA® is someone who comes from a financial planning, accounting or legal background and goes through an intensive training program to become skilled in analyzing and providing expertise related to the financial issues of divorce. The CDFA® (Certified Divorce Financial Analyst®) :

- Becomes part of the divorce team, providing litigation support for the lawyer and client, or becomes a member of a Collaborative Law team. In either event, the CDFA® will be responsible for:

- Identifying the short-term and long-term effects of dividing property.

- Integrating tax issues.

- Analyzing pension and retirement plan issues.

- Determining if the client can afford the matrimonial home – and if not, what might be an affordable alternative.

- Evaluating the client’s insurance needs.

- Establishing assumptions for projecting inflation and rates of return.

- Bringing an innovative and creative approach to settling cases.

The Certified Divorce Financial Analyst® also:

- Provides the client and lawyer with data that shows the financial effect of any given divorce settlement.

- Appears as an expert witness if the case should go to court, or in mediation or arbitration proceedings.

- Is familiar with tax issues that apply to divorce.

- Has background knowledge of the legal issues in divorce.

- Is trained to interview clients so as to:

- Collect financial and expense data.

- Help client’s identify their future financial goals.

- Develop a budget.

- Set retirement objectives.

- Determine how much risk they are willing to take with their investments.

- Identify what kind of life style they want.

- Determine the costs of their children’s education.

How A CDFA® (Certified Divorce Financial Analyst®) Can Help A Divorcing Couple

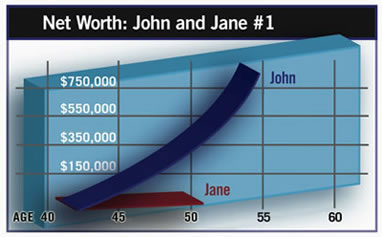

John and Jane are 40 years old and have two children. They own a home worth $165,000 with a net equity of $77,500. Their retirement savings total $165,500. John earns $90,000 a year and has a take-home pay of $68,760 a year. Jane has never worked outside the home and has no job skills, but hopes to get a part-time job with take-home pay of $8,900 a year.

The following settlement has been suggested. After the divorce, Jane and the children will live in the matrimonial home, which will be deeded to her. She will also receive $44,000 of the retirement savings while John will receive the remaining $121,500, thus dividing the assets equally. John will pay Jane spousal support of $600 per month for five years and child support of $225 per month per child. He will also pay the children’s college costs, starting in four years.

John’s expenses include his normal living expenses, child support, spousal support and education costs. Jane’s expenses include support for the children, and will be reduced as each child leaves home to attend college.

At first glance, this appears to be a reasonably fair settlement. However, a detailed analysis creates the financial future illustrated in Graph 1 (below). As you can see, Jane’s assets will be completely depleted within seven years, whereas John’s investments will grow dramatically.

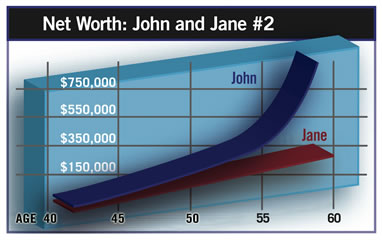

To improve Jane’s financial future, an alternative settlement could provide her with increased spousal support of $1,500 per month for 10 years – which would actually cost John $1,005 per month in after-tax dollars.The correct child support for two children according to the Child Support Guidelines in their area is $1,136 per month for a payor with John’s income. Jane could also be awarded an additional $24,300 from the retirement savings plans, although she might need to cut her expenses by 10%. These changes in the original settlement would produce the results illustrated in Graph 2 (below). If they are made, John will still have a surplus, which he can add to his investments. If John stays within his budget and invests all of his extra income, his investments have the capacity to grow to $2.5 million by the time he is 60.

This example illustrates the value of financial planning as a means of reaching a more equitable divorce settlement. If the court’s intent is to treat both parties in a divorce as equitably as possible, it is essential to analyze the marriage as if it were a financial contract, and a CDFA® is uniquely suited to do so.